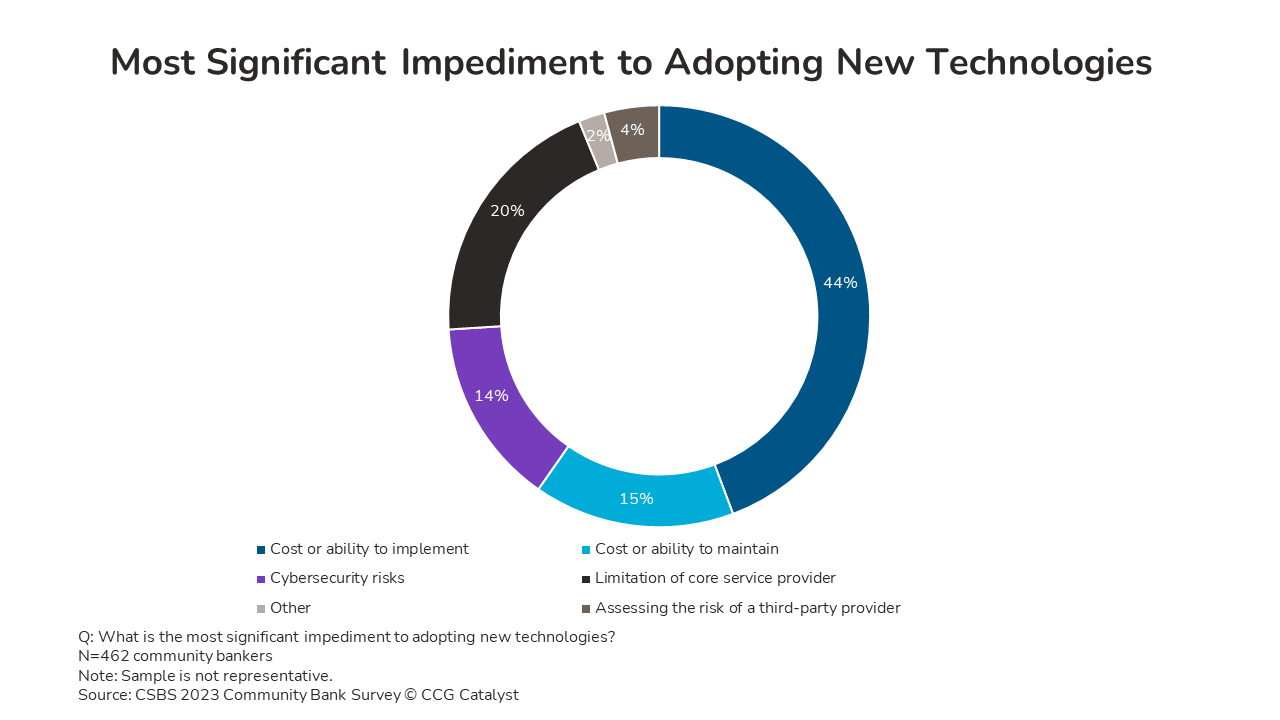

This sample’s emphasis on cost and implementation suggests that for many community banks, new technology is too pricey or complex to try. As we’ve written, the cost of maintaining existing technology can overwhelm budgets, leaving little left for improving a bank’s systems; the monolithic, fragile nature of aging technology means that substantial changes introduce risks that some bankers find too high. These factors can put a bank in a technology rut, threatening its relevance and perhaps even long-term survival.

A question bankers should ask is how they might escape enough of the maintenance burden to transform their bank — if only gradually. They have several broad options to migrate to more flexible, cost-efficient systems. How appropriate a choice is depends on the magnitude of technical challenges the bank faces, its appetite for large-scale change, and its ability to afford the upfront and ongoing expenses. It’s no surprise that, according to CCG Catalyst research, respondents tend to prefer middleware or gradual migration via upgrades to enterprise applications.

Bankers first need to understand the technology they have, product options given their current state, and the governance in place for the bank’s systems. With a firm grasp on those capabilities and constraints, they can take a realistic approach to their technology strategy and practices. As we’ve noted, a bank’s approach to technology strikes an appropriate balance between maintenance and modernization. Technical competence from senior leadership on down will help the organization find that balance.

With realistic expectations, the board can articulate a vision for modernization, set a reasonable risk tolerance, sketch out a technology strategy, and take a holistic view on what needs to change versus what can change. Some bankers may feel stuck, but creative thinking, patient planning, and gradual change should eventually take them where they need to be. The worst position they can find themselves in is a “head-in-the-sand” attitude — which makes it easy to give up on modernization before it starts.

Banks may only be able to take small steps with technology due to cost or integration challenges. But hanging onto customers with growing expectations for the experience takes proactive work. Doing what and in which order will take further thought. It will be unique to a bank’s current state, its business strategy, and how far it’s willing to go with modernization, today and in the long term.