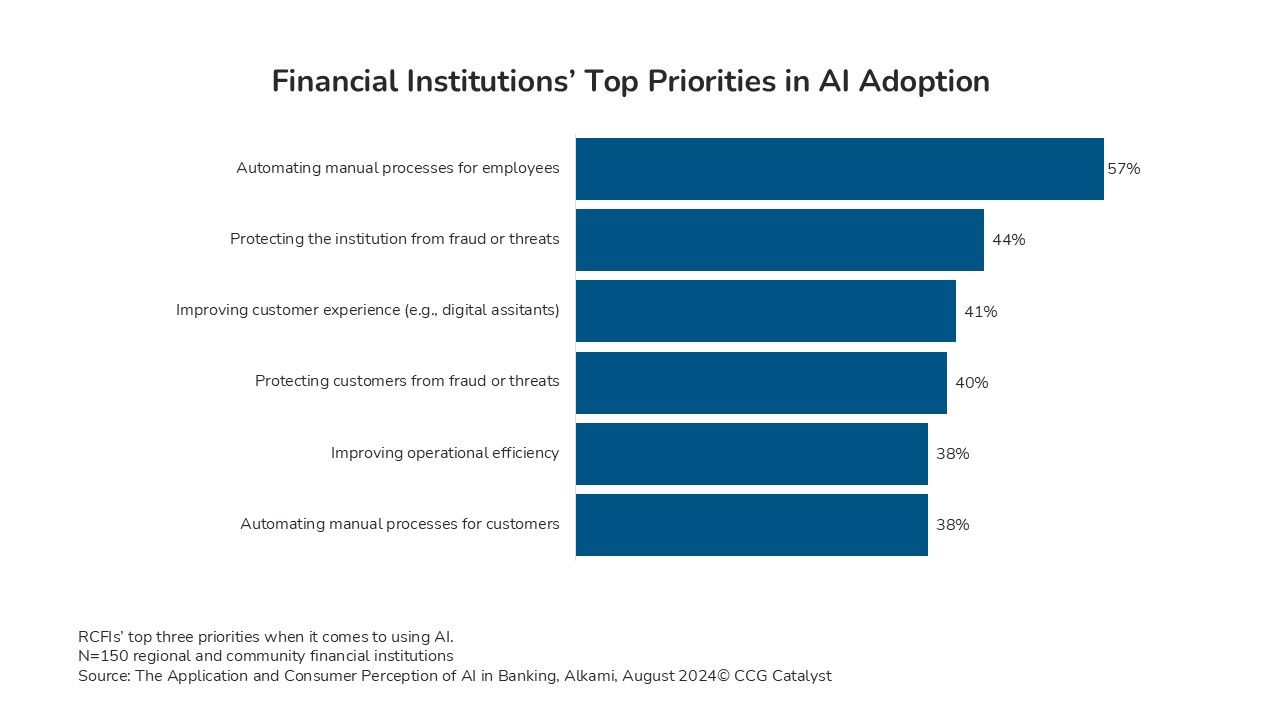

The most common priority for AI adoption among a sample of financial institutions (FIs) in a study by Alkami was automating manual processes for employees. Within that group, which included both banks and credit unions, 57% ranked it as a top three priority. It was 13 points ahead of protecting the institution from fraud or threats. Improving the customer experience came in a close third.

As we wrote, bankers may be more comfortable with applications for AI that are familiar, have relatively low risk, or for which the cost of a mistake is relatively low. “Familiar” and “relatively low risk” are related and include the longstanding use of machine learning to do things like detect fraud or money laundering or for routing customer concerns via virtual assistants.

Most banks should keep their focus on accepted use cases for AI like those highlighted in the study. Instead of being flashy and new, these use cases are just becoming more sophisticated. Groundbreaking or unfamiliar use cases should stay on a slower track as bankers better understand the technology, assess their own risk tolerance for AI-driven tools, and create frameworks for risk mitigation and compliance.

Among the top three options selected in the survey:

Back-office operations are an immense amount of work for FIs and many tasks can be automated. Data entry and document management are two often-manual tasks that back-office staff are better off handing to computers. Robotic process automation, for example, has use cases in banking that include document reading and application processing, bringing many different sources of information together often requiring manual reviews. The ideal outcome for cost and efficiency is straight-through processing.

As security threats become more complex, so must FIs’ defenses against them both with regards to keeping customers secure and maintaining the integrity of the banks’ systems. On the customer side, AI-driven security measures can bar unauthorized access to account information and payment initiation. AI can recognize suspicious transactions, conduct biometric authentication, and determine authorized behavior based on patterns. Internally, AI may help reduce liability to the bank and anticipate and react to threats.

Use cases for AI in banking from a customer’s perspective are often related to the experience, including machine learning-driven financial insights and recommendations, personalized shopping for financial products, and conversational assistants. Generative AI could in theory augment this experience with more fluid responses to customer inquiries and computer-generated, individualized marketing.

As we wrote, bankers should keep their scope in check. “What’s our AI strategy?” is too broad for most banks, and it’s more practical to ask, “what’s our modernization strategy,” “what tactical steps should we take to modernize,” and “what do modern solutions need to be successful in our environment?” The discussion turns to the solutions for concrete problems that AI enables, where and when those solutions can realistically be deployed, and barriers to the use of that technology.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.