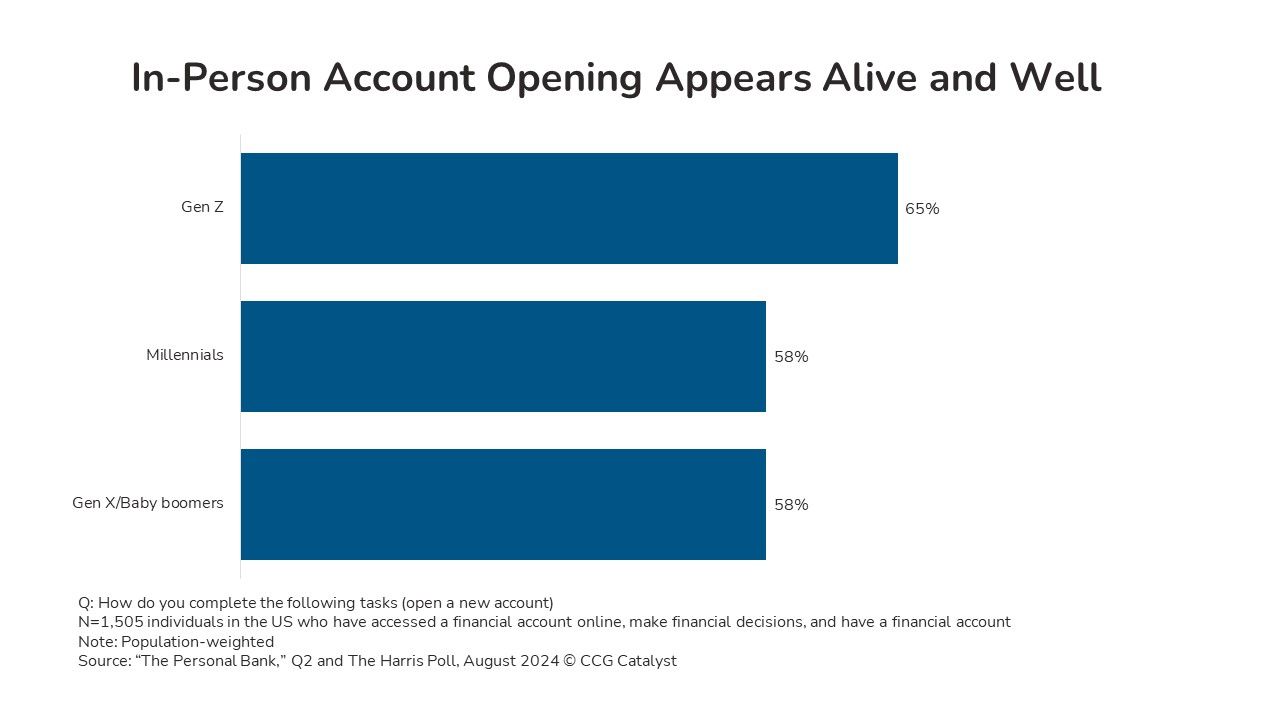

According to a recent Q2 and Harris Poll survey, 65% of Gen Zers and 58% each of millennials and Gen Xers/baby boomers (combined) said they would open a new account in person. These results matter because of the sheer overall demand for in-person account opening and the especially high demand from Gen Zers. The number for Gen Z could once have been chalked up to that demographic’s lack of experience with banking and its need for advice. But as Gen Zers age, that story may not stick.

Gen Zers, now aged between 12 and 27 years old, include millions of consumers who have been legally able to open a bank account for years. Changes to banking channel use, including mobile’s growth into the most frequently used way consumers manage their bank account (as we’ve covered), haven’t erased legacy channels’ value to acquiring, engaging, and retaining customers. Financial institutions (FIs) must invest wisely in front-office features and functions with the most value to their customers, both in digital channels and in person.

When consumers use a channel for a focused range of tasks, it deserves attention — channels that do everything all the time are probably bloated. To make the right investments in channels, FIs must understand what customers will want, when, and where’s they’ll want to get it. In the context of account opening, it’s about what they’ll buy next — Gen Zers, for example, will need more non-depository products as their financial situation and life stage demand it. The FI where they first opened an account has an opportunity to make that sale, but so does any other bank with attractive products and a competitive account opening journey.

As we’ve written, physical channels and digital channels should complement one another. FIs need an omnichannel strategy that anticipates their customers’ behaviors, expectations, and needs over time and in any context. While a branch may be the preferred channel in general to open an account, it may also be part of an omnichannel journey. It could touch mobile or online banking, the branch, or another channel — between a customer’s research phase to starting an application, submitting an application, and getting it approved. It’s important to be able to pick up this journey from one channel to another.

A branch with the strongest business case likely focuses services on customers’ primary use cases. With mobile’s dominance in day-to-day banking, in many cases branch strategy should emphasize certain types of in-person interactions (like account opening, according to the Q2/Harris Poll data) and continuity with digital channels. A branch that’s attractive and efficient for customers who use digital for day-to-day tasks has long-term value. Bankers should think about how to design branches so that they’re best suited for tasks other channels aren’t well-equipped to solve and calibrated to customer demand.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.