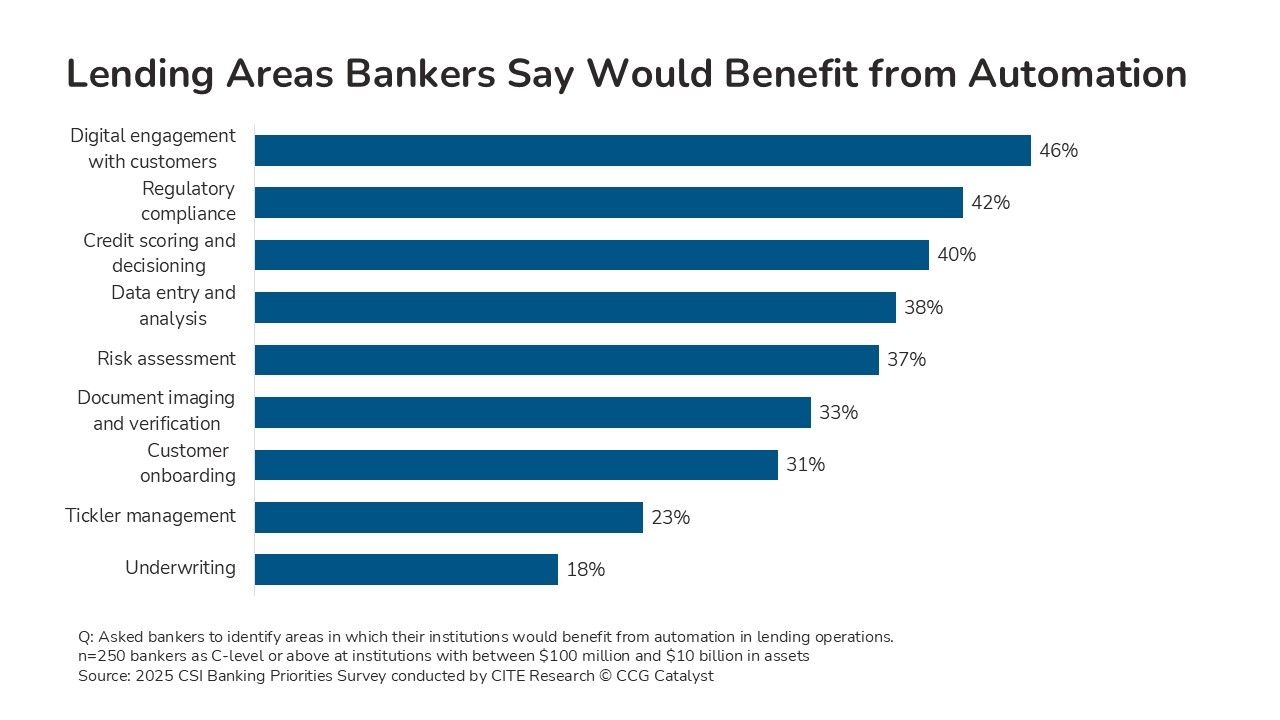

In our discussions with bankers, efficiency and automation in lending keep coming up. Automation should augment and improve what humans can do and increase their capacity. It should also make self-service channels more effective. In the CSI 2025 Banking Priorities Survey, digital engagement with customers topped the list of lending areas bankers said would benefit from automation, picked by 46% of respondents. That was followed by regulatory compliance and credit scoring and decisioning.

Here’s a look at how these areas might profit from automation:

Digital channels are automated in the sense that users don’t need human bankers to conduct basic tasks. But there are opportunities to go beyond that. For example, customers may receive immediate offers for products in context. Or when a customer fills out a digital loan application, a virtual assistant may answer questions and route topics to agents at a contact center. On the agent side, it may create context for the inquiry in real time based on customer information and activity, predicting immediate needs.

Regulatory compliance is a human task that automation can streamline. Modern governance, risk, and compliance solutions may manage compliance polices, suggest policy changes to match emerging standards, produce reports and file them with regulators, and simplify the audit process. An AI copilot and no-code interface could make it quicker for risk and compliance employees to tweak settings and reduce the burden on IT of managing it. (Integrated risk management software also applies to cyber risk, which is increasingly top of mind.)

Credit scoring and decisioning is evolving with more, better data sources and machine learning-driven decisioning engines. Traditional credit scores, using a FICO score or similar, are already automated based on a credit scoring model and data from consumer credit reports. Now, automated cash flow-based approval is increasingly possible as open banking enables the connection of more financial data sources. But it and other new approaches need substantial data handling and analytics capabilities to work efficiently. Ideally, decisioning is straight-through nearly all of the time with certain cases subject to human review.

Lending automation isn’t limited to these top three items — it has a role in other areas like document imaging and verification, application, origination, and onboarding workflows, customer follow-ups, and underwriting. Progress with automation in any of these areas reduces manual tasks and minimizes human mistakes and inconsistent judgements, reducing the headcount needed to run a risk-conscious and profitable lending business. It may also improve the customer experience by accelerating the pace of loan origination.

Bankers need to think about the investments they should make to modernize their lending operations and what they’re willing to wait for from their core provider. Legacy point solutions handle basic digital, compliance, and decisioning tasks but are built for another era. Vendors now advertise platforms that integrate functions throughout the loan lifecycle, minimize the work that goes into the lending process, and enable the integration of best of breed applications. But data availability is still a problem. Siloes limit automation and fixing them is bigger than a single product line.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.