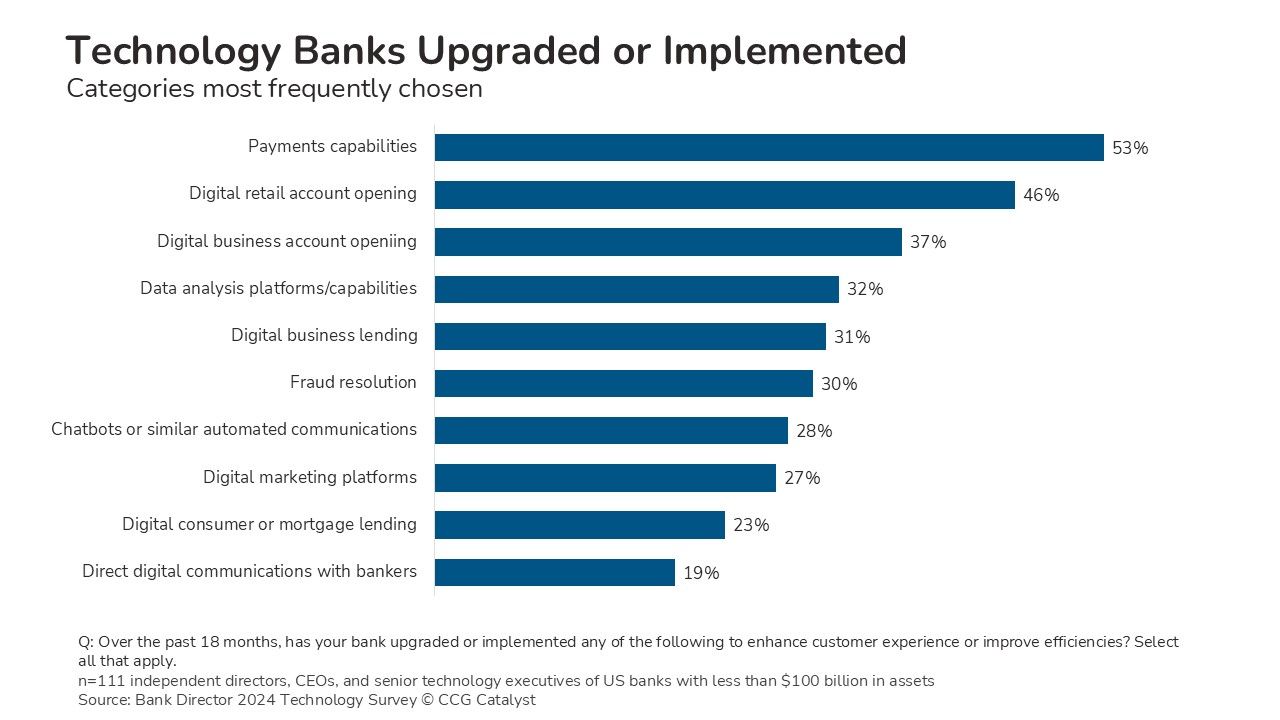

Over the past 18 months, 53% of bankers surveyed had upgraded or implemented payments capabilities to enhance customer experience or improve efficiencies, according to a Bank Director survey.

This high proportion is not a big surprise given the drive for payments modernization in three respects:

Real-time payments: FedNow adoption has grown from 35 early adopters in 2023 to about 1,300 participants. RTP has grown from six early adopters in 2017 to nearly 900 today. Joining a real-time payments network is quickly becoming a competitive need as adoption spreads beyond the largest institutions to community banks and credit unions. Participation takes more than flipping a switch: institutions may implement a new payment module via their core’s abstraction layer or make bigger changes to their payments architecture.

P2P support: Zelle has spread dramatically since its launch in 2017, to about 2,200 participants, but that leaves thousands of others without modern, integrated P2P capabilities within digital banking. Institutions may perhaps be evaluating their strategic interest and the costs versus the benefits to customer experience and stickiness. However, many institutions have held back — in our research, we find some banks instead focusing on APIs that play well with third-party apps like Venmo and Cash App (a quasi-payments use case, requiring upgrades to the digital banking platform or the core).

Overall infrastructure: The adoption of new or nearly new payment rails is nudging institutions to rethink their overall payments architecture. As we’ve written, banks are increasingly moving beyond legacy enterprise payment hubs — often bundled with core systems — to cloud-native third-party solutions that intelligently orchestrate payments along multiple rails. These modern hubs typically include fraud detection, analytics, and modern APIs that support the integration of best of breed tools.

Transformative upgrades to payments technology aren’t “one and done.” Real-time retail payments could be a paradigm shift in how smaller transactions are sent and received between financial institutions. But first they need to do both — in our research, we’ve found that “receive” is more palatable and more common because of concerns about account takeover fraud for “send,” although as we’ve written, those may be overblown.

Another challenge for payments modernization, as with innovation in other classes of bank technology, is making a careful strategic assessment. Other disruptive payments infrastructure may be just over the horizon — chatter about stablecoins for cross-border payments and tokenized deposits, for example, has risen markedly over the past year. Stablecoin advocacy is quieter than the “decentralized finance will reinvent the financial system” ideology linked to the crypto bubble but may also represent a “shiny object.”

For financial institutions, payments modernization will be a multi-year journey, shaped by strategic decisions about technology, a deep understanding of customer expectations, and attention to the changes in the competitive landscape. We may continue to see upgrades to payment technology as banks and credit unions adopt real-time payments, as those capabilities become more sophisticated, and as payments infrastructure evolves.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.