Addressing Scale Challenges in Risk and Compliance

Addressing Scale Challenges in Risk and Compliance

SEPTEMBER 5, 2024

By: Tyler Brown

Bank Technology and Data

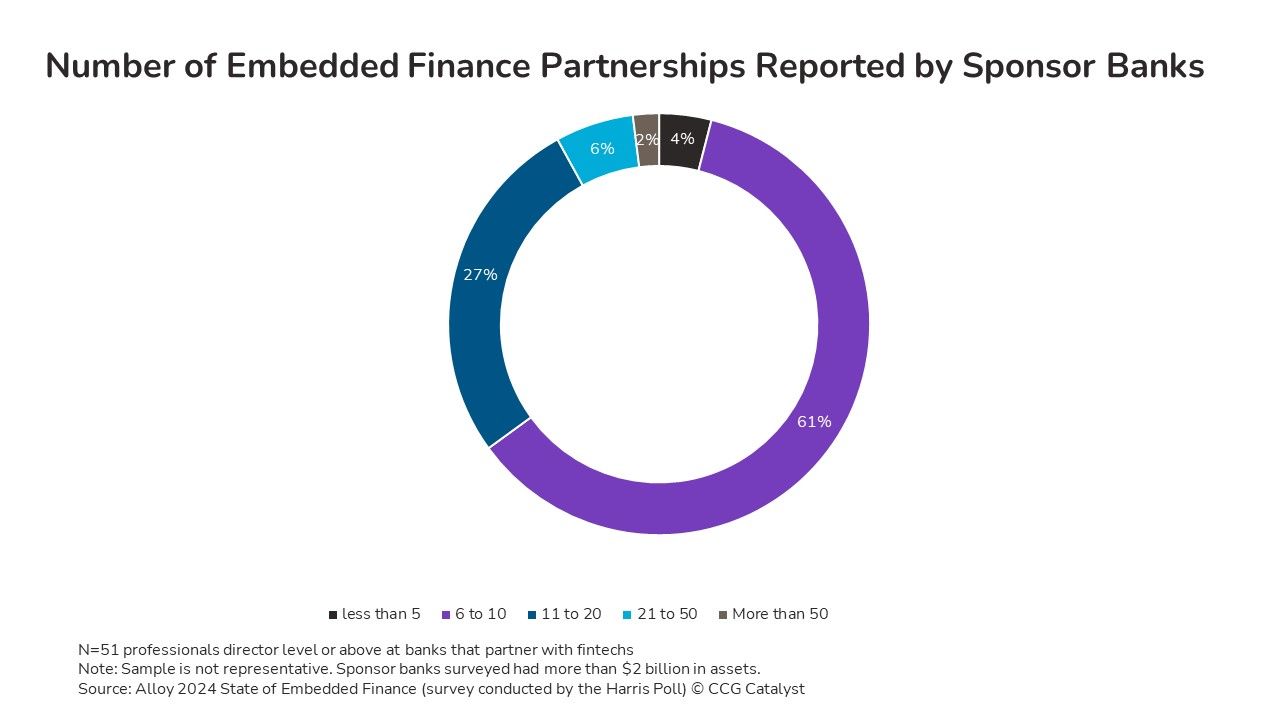

Operating a robust compliance program gets harder as a financial institution (FI) grows in size and complexity. As we’ve written, those challenges multiply when that FI expands beyond direct channels to third-party partners that are responsible for acquiring and directly overseeing end customers. Amid enforcement actions and proposed regulation, perhaps it’s counterintuitive that a survey from Alloy fielded early this summer found that 61% of 51 respondents from a sample of Banking-as-a-Service (BaaS) sponsor banks with more than $2 billion in assets reported six to ten partnerships and another 27% reported 11 to 20.

These BaaS (referred to in the study as embedded finance) partnerships are a lot for a bank’s risk and compliance teams to handle, particularly in the community-bank segment. Banks that depend on manual processes and the sheer size of their risk and compliance teams to mitigate potential problems introduce fixed costs that a sponsor bank may be unwilling or unable to bear. Suboptimal compliance practices — passing spreadsheets back and forth between the bank and partners, doing manual reviews, and conducting periodic but only occasional audits — cause delays, lag the high growth typical of BaaS partnerships, and introduce additional risk.

Enter the idea of programmatic compliance orchestration. It in theory makes managing partner compliance more efficient and cost-effective (it’s offered by at least several providers, and we’ve touched on it before). From the bank’s perspective, it means real-time oversight of partners’ compliance policies and practices and the ability to adjust and enforce policies in near-real time. It also means that, ideally, a platform doesn’t require programming expertise, and the risk and compliance teams can make changes with little to no back-and-forth with the IT team, avoiding lengthy in-house development cycles.

Risk management and compliance orchestration extends to platform integrations, including the data sources banks use in risk decisioning and point solutions that may provide certain functions, like monitoring for AML compliance or KYC, for example. The outputs flow downstream from the bank to program partners to provide parameters for policies, visibility into outcomes based on those policies, and the ability to make quick changes.

As we’ve written, and as Parilee Wang, chief product officer at Alloy, reiterated in an interview with CCG Catalyst, there’s a balance sponsor banks need to strike between responsible growth and innovation. As the cost of compliance for sponsor banks grows, some will make the right investments in oversight and control. Others that aren’t willing to commit will exit or scale down BaaS, or in the context of new entrants, never start a program. To create a healthy long-term BaaS ecosystem, that’s for the best.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.