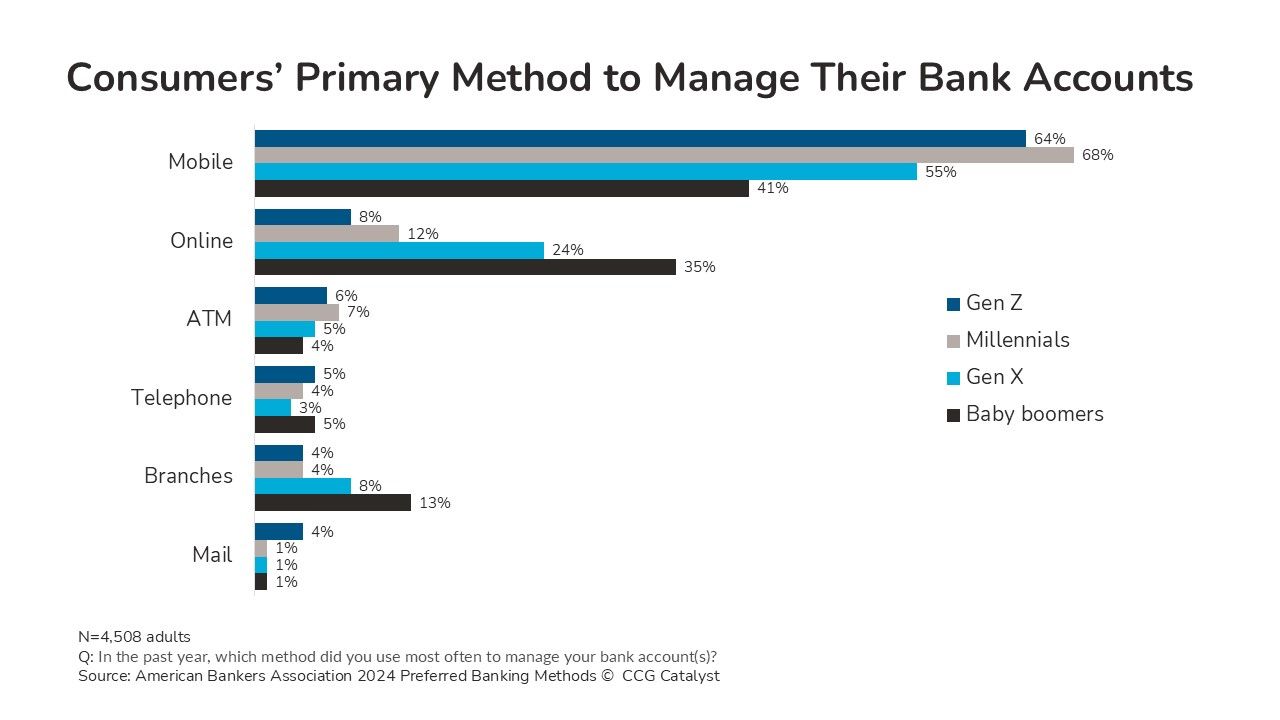

It’s well-documented that mobile is the primary or preferred banking channel for Gen Z and millennial consumers, and that digital overall dominates consumers’ interactions with their bank. According to an American Bankers Association survey, the most-used banking method for 64% of Gen Zers and 68% of millennials is mobile. The vast majority for each generation measured is digital.

Bankers should ask the question: Why measure primary channel at all? It’s clear that other channels’ importance for day-to-day banking tasks has receded. Better to ask which features are most important to a channel and how to optimize investment in each to serve those functions. A clear part of that approach is spending on a consistent and complete digital experience. Another piece is trimming and retooling alternative channels.

The details depend on a bank’s business strategy, but here are a few considerations:

The digital experience should be consistent between mobile and online. Digital may be formatted to fit different platforms, but available features should be substantially identical based on what financial information customers need to know, at what cadence, and the actions they need to take on it. There’s no good reason for mobile and online to be siloed.

The branch, as we wrote, should focus on high-value interactions defined by return on investment — driven by customer demand and the value of a product or service to a bank’s bottom line. That includes continuity with digital channels but also uniquely in-person services that aren’t easy to deliver via digital.

Basic services provided through digital shouldn’t necessarily be duplicated in another channel. Digital and particularly mobile have features that customers want to use quickly or briefly, like basic account information, for example, balance and transaction history, or basic money-movement tasks.

Digital with basic features should add functionality that doesn’t make sense in other channels. Certain features are digital-only (or at least digital-first), like managing card settings, chatting with a virtual assistant or customer service representative, accessing a credit score, or tracking personal financial trends.

Bankers need a channel strategy to make sure that investment is tied to business value. The answer to meeting evolving customer needs and expectations for touchpoints is not to add one more channel to what already exists or duplicate what’s already available. It’s to choose the best channels for certain functions, invest in them, and prioritize what matters to customers. “All of the above” is not a worthwhile approach. As with most things, bank leadership needs to be thoughtful and deliberate to drive favorable outcomes.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.