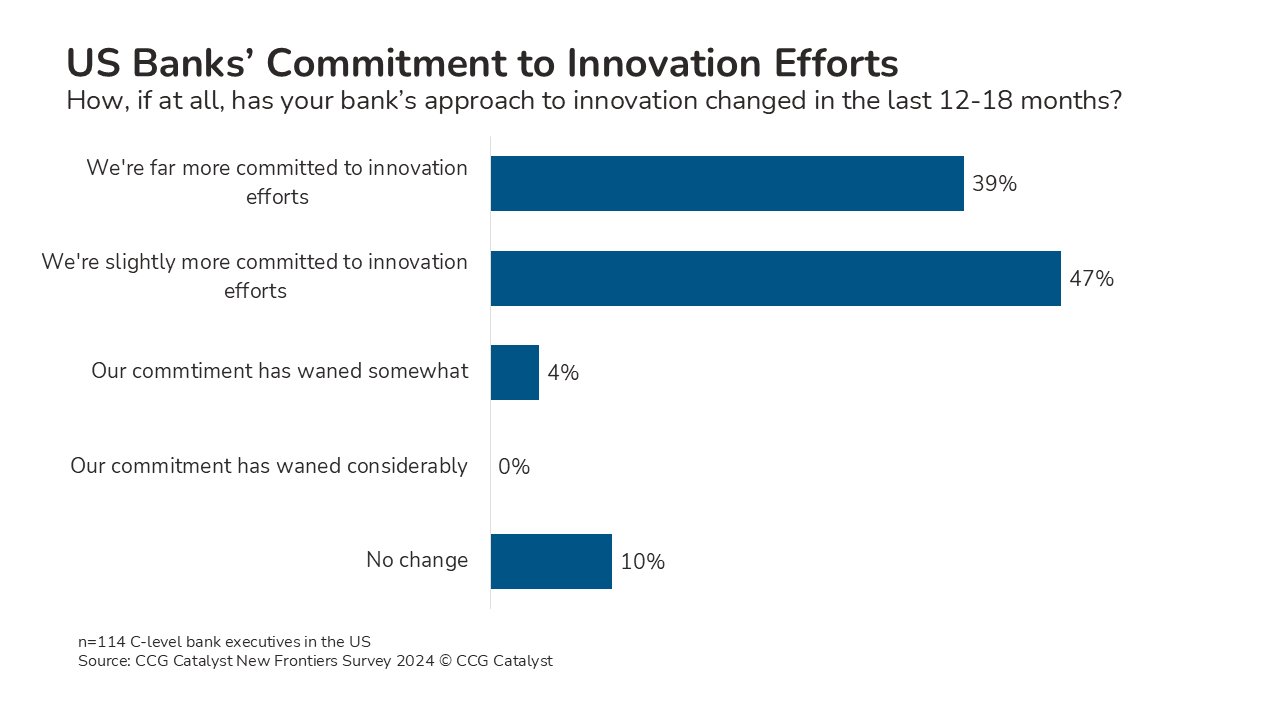

Nearly 90% of bankers in our New Frontiers 2024 survey said they were slightly or far more committed to innovation than in the last 12-18 months. But commitment to innovation doesn’t always have business impact, and even when it does, efforts may be misdirected. Innovation may just be a word, and bets on innovative business models like Banking-as-a-Service and crypto, for example, have in many cases fallen short of lofty expectations. In response, bankers have markedly pulled back from such innovations, had to rethink what innovation means to them, and how to approach it responsibly.

Bankers’ greater commitment to innovation combined with anecdotal evidence that many have pulled back from new ways of doing business may come from how bankers define “innovation” and “commitment.” In many contexts, the term “innovation” suggests dramatic changes to technology or business choices over a short period of time that put the innovator far ahead of its market. It can be hard for bankers to make the leaps to large-scale change, and they may mistake iteration — which is much safer — for innovation. Not defining innovation well makes it difficult to commit to it.

To accurately define innovation, understand its implications, and act on it, bankers will need to avoid platitudes and keep their focus on what matters most to their bank’s success. Froth around flashy technology and chatter about poorly understood buzzwords may sway board meetings away from business fundamentals. Successful innovation of any kind is ultimately a product of business strategy — careful boards think backward from concrete business outcomes to the technology and operations that will support them.

Instead of asking, “What is our innovation strategy?” boards may want to ask, “What business metrics should we move, and how will we move them?” Broad options include growth of the business and greater efficiency — which may not be tied directly to a novel business model or radically new technology. To the extent that business choices enable attracting deposits, expanding the loan book, and sourcing fee income — and technology choices help manage long-run costs — novel approaches may be warranted. Bankers must measure their returns effectively and manage risk, compliance, and governance.

Innovation in most corners of banking moves slowly because it must. Shiny objects — ideas that are popular but don’t have a robust risk-mitigated business case — are the biggest pitfall. A greater commitment to innovation for most banks will likely mean being unafraid to consider new things in their business planning and the dedicated pursuit of transformational projects and business choices that are outside the norm.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.