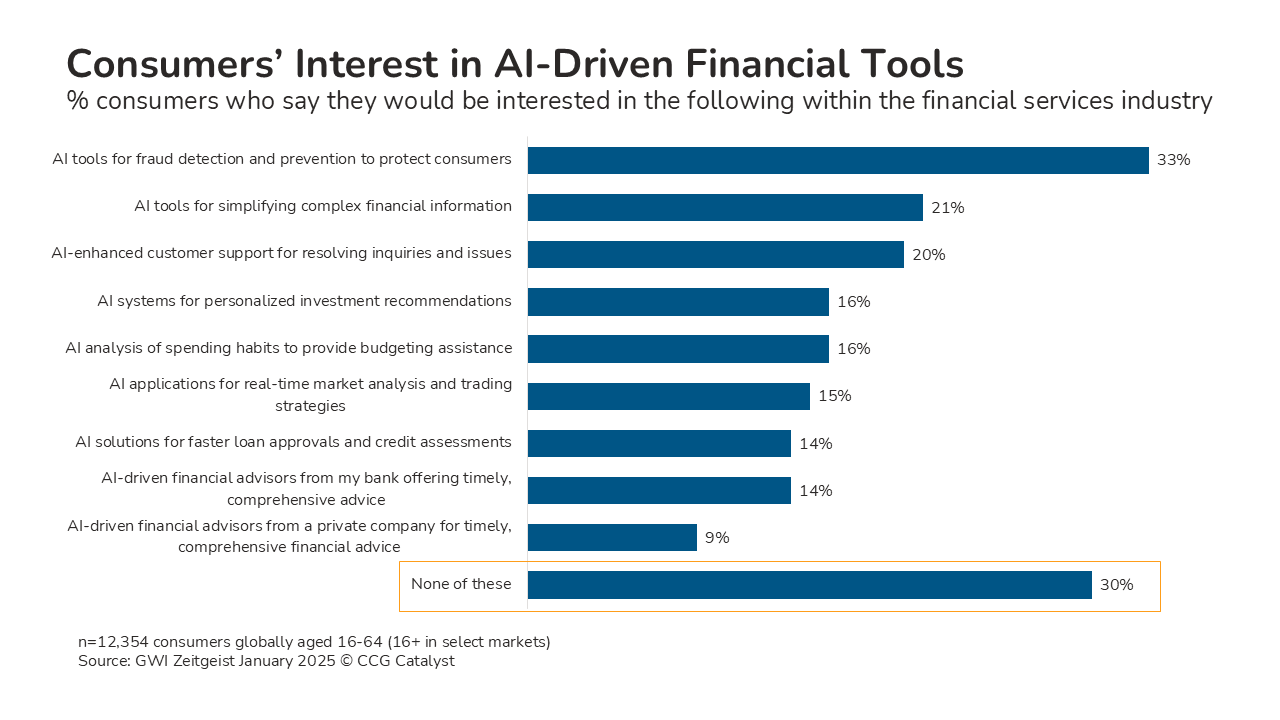

Bank customers may not care all that much about AI. In fact, in the latest GWI Money Talks Report, 30% of consumers surveyed said none out of nine options for AI applications in financial services would be of interest to them. The most-selected option of interest was AI tools for fraud detection and prevention to protect consumers, but only a third of respondents chose it, and no other choice garnered interest from even a quarter of the group. The survey results raise questions about which tools and features consumers want from their financial providers and how AI might be relevant to them.

There doesn’t seem to be any concise public narrative around how AI can complement consumers’ financial lives. As such, it’s likely hard for consumers to see how AI would be useful for specific applications within financial services. Should they expect AI to enhance their experience? Could it introduce unnecessary risks? Respondents who picked “none of these” might see dangers related to AI in financial products or not see its relevance at all. However, the bigger insight from this data is likely about more than AI, instead pointing to an important comment on what drives customer interest: Customers generally don’t care all that much about enabling technology, they care about outcomes.

Consumers have good reason to demand sophisticated fraud detection and prevention, simplified financial information, and enhanced customer support — to name consumers’ top picks in the survey results. Whether AI has anything to do with those features may be beside the point for the user, even when truly unique or useful features are “AI-enabled” or “AI-driven.” Will AI influence how consumers perceive financial features’ usefulness? Under the hood, perhaps. But any talk about AI needs to come from an exercise in strategic thinking about customer needs and what the institution intends to deliver.

Bankers focused on business impact will work backwards from customer needs to customer experience — and only then will they arrive at technical solutions. There’s little reason to assume that a certain type of technology will solve customer needs — and that can be an even bigger problem when the technology itself is poorly understood. Sometimes, bankers don’t even know how to talk about AI or why it’s important in the first place. That raises the risk that “shiny object syndrome” instead of a business case will drive technology strategy and selection.

After bankers establish a customer need that an AI-driven product will best fulfill, their focus on AI itself should be on due diligence and risk assessment. Regulators have articulated risks and the potential compliance burden of AI use in banking, and bankers should understand them well if they’re going to use AI-enabled tools at all. This sober approach to AI prevents institutions from jumping on board with unfamiliar technology and keeps the board and senior management’s focus on what fits the institution’s business model and risk tolerance.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.