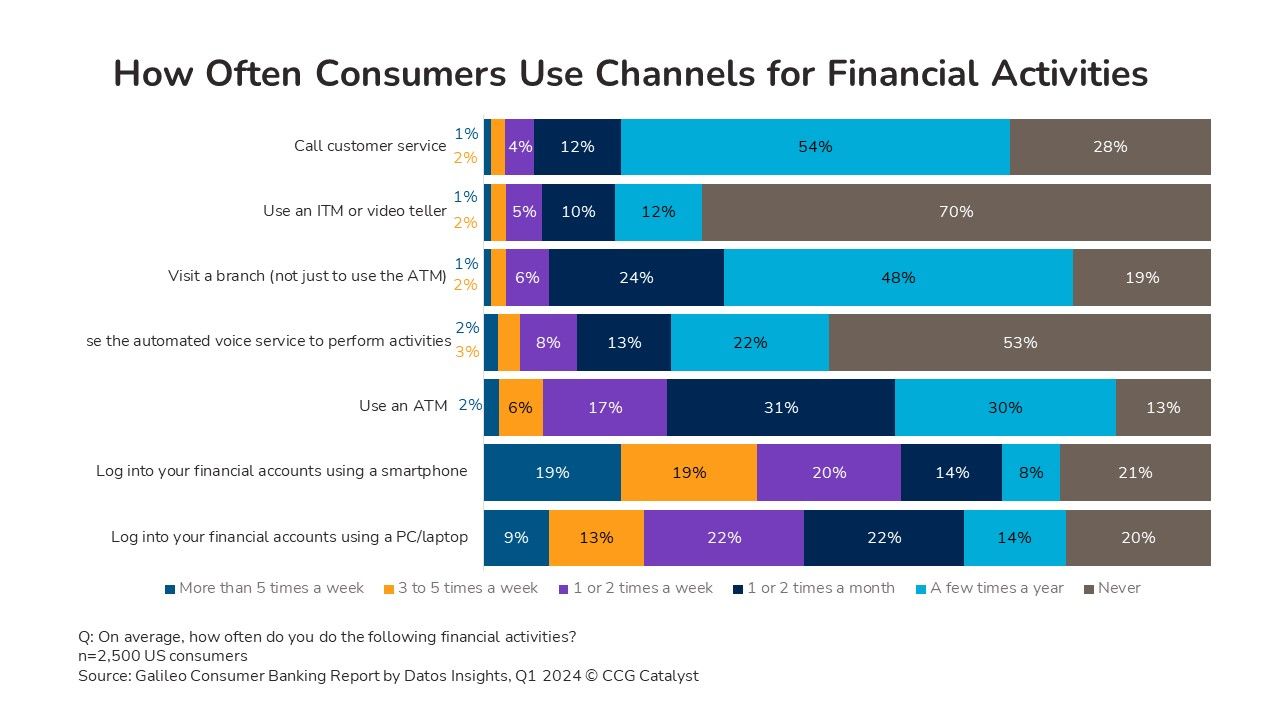

By wide margins, consumers most frequently conduct given financial activities via their smartphone, according to research from Galileo: 58% used their smartphone to log into their financial accounts at least weekly and 19% used mobile to log into their financial accounts more than five times per week. In contrast, consumers are likely to use an ATM or visit a branch no more than a few times a month, if not further apart.

Bankers may be tempted to think about this data in the context of a general decline in the use of nondigital channels and the increasing dominance of mobile. But it’s worth some nuance as they reevaluate their channel strategies. There are channels in permanent decline or that never took off, and here are those that consumers clearly need and use, but in which the nature of customer interactions is changing. The channels clearly out of favor are interactive teller machines (ITMs) and automated voice services (IVRs) — whose utility for banking tasks is marginal compared to channels that fulfill similar basic functions.

The biggest warning sign for a channel should be when a critical mass of consumers say they never use it. The ATM and its variants, for example, are probably most useful for cash deposits, withdrawals, and balance checks; using an ITM to speak with a teller adds little value if any. Completing tasks with automated banking over the telephone is more easily done in digital banking and with less wait time. Regular but less frequent use is a different challenge and opportunity.

Channel use “monthly” or “a few times a year” means that banks should encourage customer interactions optimized for the channel and not doable at a lower cost for the bank or at greater value to the customer. For example, there’s little value in the branch as a place to deposit or withdraw money per se. But it’s a storefront for the bank’s brand, a backstop for customer problems and questions, and an opportunity for the bank to sell complex products and advisory services to customers. For some communities, it may also serve as a social center.

The key lessons for bankers may be that a) some channel “innovations” are trying too hard to do something new and b) channels for their own sake aren’t the best way to think about touchpoints. A different model would be to score an interaction with a customer by cost to both the customer and the bank and that interaction’s impact on the relationship. A high-cost branch interaction, for example, should materially strengthen the customer bond or fit into the sales cycle of a high-margin, sticky product. A mobile interaction will more likely be perfunctory but also virtually cost-free — like a balance check, a transaction review, or an electronic payment.

Bankers should think about touchpoints with that equation in mind. A huge barrier to channel reevaluation and innovation is inertia — because a channel exists, it will continue to exist as it always has, with incremental and perhaps even nonsensical changes. Like with leading-edge innovations, senior leaderships need to start with their business strategy and then focus on what channel choices will best fulfill that strategy given their customer base.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.