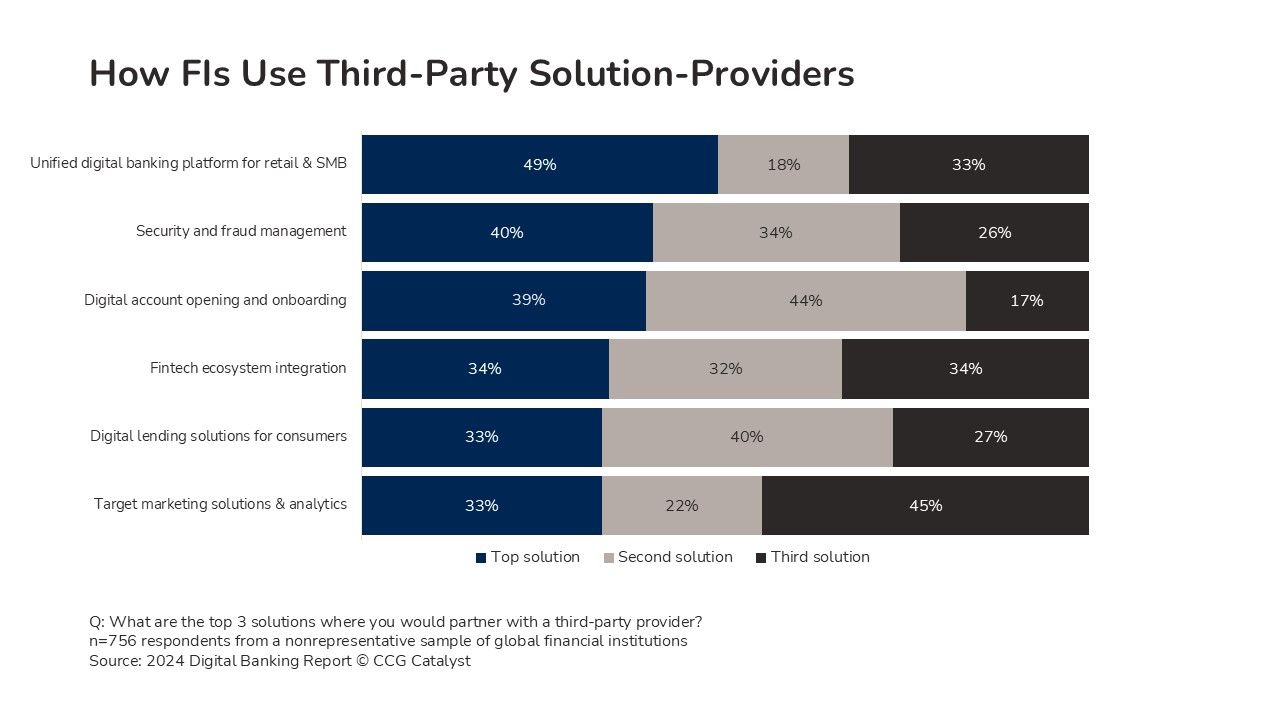

A sample of financial institutions (FIs) globally most often picked a unified digital banking platform for retail and small and medium-sized businesses when asked to choose the top solution they would partner with a third-party solution provider for. Security and fraud management and digital account opening came in neck-and-neck for second place. The results were based on responses to the 2024 Retail Banking Trends and Priorities Report.

These survey responses paint a partial picture of the modernization issues FIs face — in the US, outsourcing is common for FIs, but internationally FIs are less likely to do so. The first tactic, often associated with a single- or minimal-vendor approach to technology, leads to single-provider issues: Dealing with technology is relatively easy when it’s dictated by one or a few solution-providers. But a limited, vendor-dependent technology roadmap probably won’t yield the highest-quality options in the face of quickly evolving third-party solutions.

The types of third-party solutions FIs in the US choose points to where they are most likely to value core-agnostic, modern solutions — taking a best-of-breed strategy for the digital experience, customer acquisition, or security, for example. To compete effectively, bankers should keep in mind how other FIs invest in their technology strategies, including the use of third-party solutions:

In the front office, enabling customer interactions across channels is important to retention and engagement amid a customer migration to digital channels and as mobile-first Gen Zers become customers. Digital account-opening and onboarding are equally important for attracting new customers through digital channels and setting them up for sticky digital services. FIs should use digital banking vendors to build a multichannel experience, ease the administration of digital banking across customer segments, and take advantage of a modern ledger. Better onboarding pushes targeted sales and cost-reduction measures.

In the back office, better security and fraud-management tools are crucial as attacks become more sophisticated, regulatory demands grow, and tools emerge to satisfy those concerns. Several sets of tasks within this realm are getting more sophisticated, driven by artificial intelligence: Transaction monitoring and AML prevention based on complex patterns; biometric authentication, including “continuous authentication” within banking sessions; and the security and integrity of the FI’s systems to avoid tampering and data breaches. Old or sporadically updated technology in the end won’t meet FIs’ needs.

A robust understanding of third-party solutions and their use in the industry are crucial to effective modernization. As we’ve written, a best of breed strategy sets the foundation for crucial long-term evolution of a bank’s tech stack. But that strategy demands a carefully planned, internally driven innovation strategy. This approach, in which FIs are free to add, remove, or upgrade third-party features and services of their choice, depends on a composable core; middleware that abstracts a legacy core; or extensible “over the top” solutions.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.