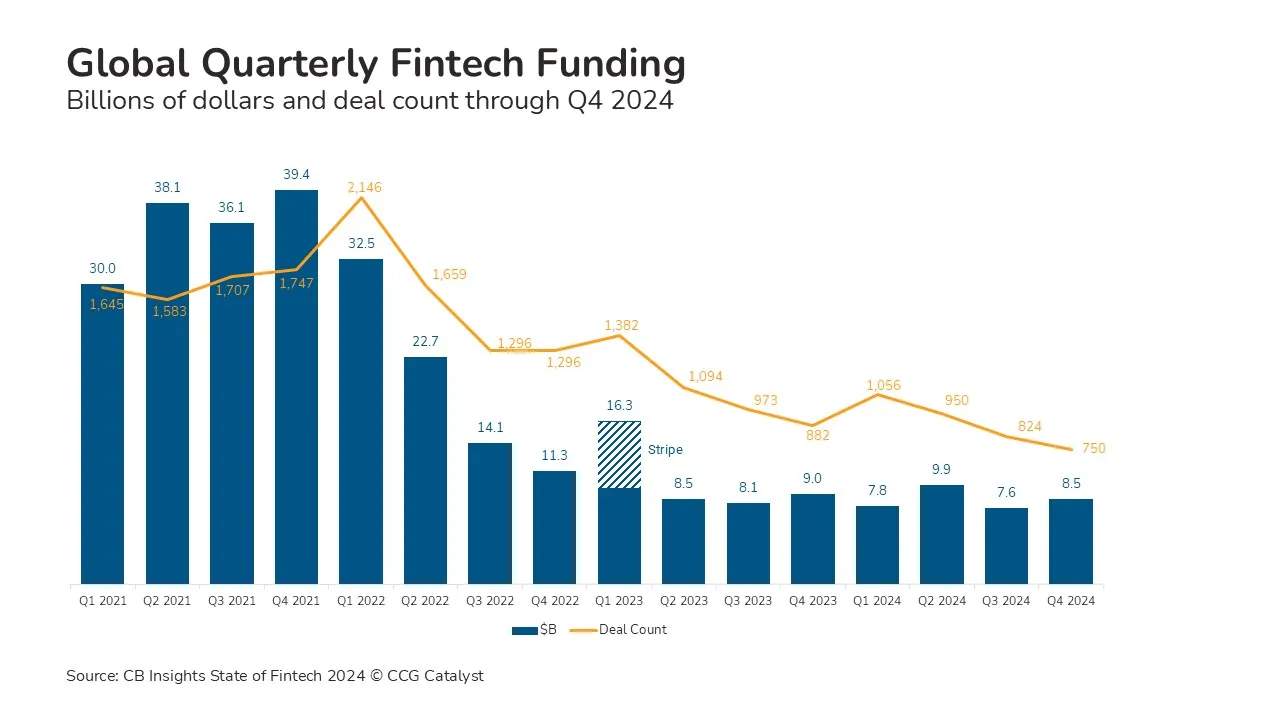

At first glance, fintech had a quiet 2024. According to CB Insights, global quarterly fintech funding ranged from $7.6 billion to $9.9 billion, between 81% and 75% below the 2021 peak. We’ve suggested that this downcycle will force fintechs to be more resilient and create investment opportunities with rational valuations. At the same time, however, muted funding may disguise potential threats to the banking industry.

Neobanks, in particular, don’t feel like the palpable threat they once did — eyepopping headlines about multibillion dollar valuations are scarce and many have left the market, especially in the US. But quietly, neobanks’ challenge to traditional banks still exists. The difference is the threat now appears to be growing concentrated within bigger names.

In Q4, two large neobanks — one based in Argentina and the other in the US — each raised hundreds of millions of dollars in equity:

Ualá, reportedly the largest startup in Argentina, raised a $300 million Series E. The mega-round was an example of strong backing for Latin American challenger banks — which include the Brazilian behemoth Nubank. Nubank occupies multiple Latin American markets and has floated expansion to the US.

Current, one of the largest domestic neobanks, raised a $200 million Series E, its first new funding since the 2021 fintech bubble. The company plans to use the money to further scale its customer base and reach profitability this year.

In April, we also noted UK neobank Monzo’s $431 million Series I and plans to attempt another big push into the US.

Large, stable neobanks at home and others that plan to enter the US market should worry bankers. Chime, Monzo, and Nubank’s parent company have all claimed a profit by some measure. Nubank’s parent company is public, and Chime is reportedly preparing for an IPO. Scale and firm financial footing make these neobanks credible challengers.

Before the fintech bubble burst, when neobanks felt like more of a threat, many financial institutions changed their products and policies to match neobanks’. The same institutions may have sighed with relief as a difficult funding environment sucked the air out of consumer fintech. But with the dust settling, the ones that remain — or are prepared to enter the US market — appear more dangerous.

Today, bankers would be wise to avoid thinking of neobank competition as a reason to jump for shiny new features. Large neobanks are shaping up to compete with incumbents of all sizes for customers — that means strategists should treat them as long-term, national competition. Given some neobanks’ diverse product offerings, they could threaten multiple sources of banks’ revenue.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.